A Closer Look at the Private Label Lending Product

While issuance volumes are nowhere near pre-crisis levels, the Private Label Residential Mortgage Backed Securities (PLRMBS) market has continued to provide access to funding for mortgage loans that don’t conform to the current tight credit markets. We observe a cycle starting in 2009 where a limited number of PLRMBS issues have made it to market through 144A rule offerings with deal volumes by vintage and origination amounts by vintage both peaking in 2017 (as of December 2017 remittance).

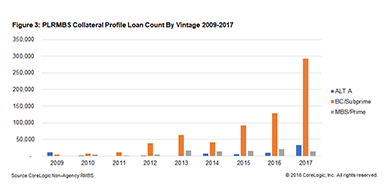

The collateral reveals the overwhelming tendency is to issue BC/Subprime deals that tend to revolve around NPL/RPL loans. These deals could include NPL/RPL portfolios being securitized from GSE auction purchases as well. Likewise, we see several legacy PLRMBS deals being called and the remaining outstanding loans re-securitized into new 144A issues. In more recent vintages starting in 2014, we’re starting to also see the emergence of a limited number of non-QM loans being included to some deals.

Issuer wise, the diversification has been significant. No less than 55 firms from 2009 to date have issued into the PLRMBS segment. However, roughly 50% of all deals issued during this time have been issued by only 5 issuers: Bayview, Sequoia, Credit Suisse, JPMorgan and Towd Point.

While the deal volumes are not comparable to pre-crisis there has been a slow but gradual resurgence the last few years. If 2015 to the present is any indication, we can expect a continued growth trend and have already reached $50B in closing balances for 2017. Going into 2018, there should be continued interest in securitizing NPL /RPL loans and further defining the evolving non-QM credit box. The question mark is with respect to the public side and whether or not we’ll see issuance under Reg AB II.

In our next installment, we’ll take a look at the traits and relative performance on the book of issued PLMBS deals between 2009 to date.

© 2018 CoreLogic, Inc. All rights reserved.

FEB